On Tuesday 20th September HMRC announced that there would be an extension to the deadline to be able to use CHIEF.

Permission to continue to use CHIEF for imports must be sought from HMRC and can be applied for here.

If you have not fully registered to make import declarations you should check if you use one that your customs clearance agent or freight forwarder has or if they will require you to do so under your businesses EORI number. Without permission to continue to use CHIEF until 31/10/2022 import entries will need to be submitted via CDS.

The Chamber’s customs agent service, ChamberCustoms, has been granted an extension to use CHIEF on behalf of customer who have not completed their set up on CDS for import entries.

Further information on how to register and more detail about the change to CDS from CHIEF is available from the Chamber here with links to HMRC guidance and how to videos.

A recording of a ChamberCustoms webinar on the switch over from CHIEF to CDS is available If you have any queries regarding requirements for setting up for CDS, about CDS generally or about the ChamberCustoms clearance agency service please get in touch with the International Team on [email protected]

From 1st October 2022 all customs import declarations into the UK must be made via the new HMRC Customs Declaration Service (CDS).

In their latest customs update email to over 3000 businesses HMRC advised that it can take some time to arrange the switch over and strongly encouraged businesses to act now to ensure that there would be no risk to consignments being held up at the beginning of October. HMRC have now released some additional guidance including how to videos to assist in setting up a business’s account.

All businesses with a UK EORI number will be registered for CDS automatically, however where there is a requirement for a business to make a payment for any VAT or duty on import clearance each business must subscribe to CDS via their government gateway account in order to be able to do this.

If a business does not already have a Government Gateway account or ID they will need to register for one.

The trader checklist is available here on the government website as a step-by-step overview of what a business needs to do to ensure that they are set up for their entries to be submitted to HMRC via CDS.

Information on the different payment methods for VAT and duty payment and how it can be managed on CDS via the government gateway account here.

Where a business uses a customs clearance agent or broker, they must set up a standing authority for their agent to act on their behalf. The standing authority can be set up via their government gateway account. How to set up a standing authority.

More information on the changes that will affect businesses caused by the swap from CHIEF to CDS and the different payment methods available via CDS please see the Chamber’s article on HMRC’s new system: CDS

If you have any questions about subscribing to CDS please get in touch with the Chamber’s International team via [email protected]

The UK has tabled new legislation, called the Northern Ireland Protocol Bill, aimed at unilaterally altering the Northern Ireland Protocol. UK Government contends that the Protocol has placed a political barrier between N. Ireland and the rest of Great Britain, and is also disrupting trade between the two.

The bill would allow the UK to override the terms of the treaty of the UK-EU negotiated Northern Ireland Protocol. We looked at why the proposal has been contentious in this article.

Key Proposal on Goods.

The proposed bill would remove the need for checks on goods travelling GB-NI, whilst maintaining full checks on EU bound goods. The propozsal introduces two coloured lanes at port to indicate which goods are destined for Northern Ireland (Green) or for the EU (Red).

The UK has provided a streamlined graphic of the proposed solution on goods below:

The proposal would based on a Trusted Trader system and shared data compliance, with fiscal penalties for those breaching the system, however the details on how this would operate, and work for non-commercial goods, is still unclear.

Major contention surrounds the use of a “Dual Regulatory” regime. UK Government argues businesses trading solely with Northern Ireland should not have to comply with EU law, and instead companies should have the choice of whether they comply with UK, EU or both, by using a UKCA, CE or both stamps.

Certain industries, such as dairy, have warned this would cause disruption on the Island if the components from one side, grain, do not meet the standards of the other, their produce, milk, will be barred market access.

In addition to this, the UK will seek to end European Court of Justice oversight, particularly on the “green lane” goods in Northern Ireland, while applying full EU law to “red lane” goods. UK Ministers will claim the ability to refer UK decisions to ECJ.

On VAT, the Treasury would be able to apply tax measures unilaterally in N. Ireland, in line with the rest of Great Britain, which it was unable to under the protocol.

A full debrief of the Northern Ireland Protocol Bill, and its impact, can be seen in this Institute for Government guide.

Wider Impact EU leaders have already said they’re planning legal action against the UK if it unilaterally acts on Northern Ireland, urging UK negotiators to return to and find a negotiated outcome. However, if the UK acts unilaterally, the EU could impose tariffs on all exports from the UK to the EU.

It is unclear what the Bill would end up saying. This piece from the UK Trade Policy Observatory (UKTPO) suggests the Bill is part of a negotiation strategy to find compromise with the EU before taking unilateral action.

The Chamber will try to keep members updated on this dynamic situation, and support where possible. The British Chambers are in regular contact with Government, if you have any comments or questions, please contact [email protected]

It’s important that businesses are aware that this change is happening in order to avoid any unwanted delays or repercussions and remain HMRC compliant when their customs declarations are submitted to HMRC via CDS.

CHIEF vs CDS

The incumbent HMRC system used for customs declarations is being taken out of service and replaced. Where entries are done on behalf of international trading businesses by brokers or freight forwarders this will not cause a change to their overall operational processes. The new system is different and will require some additional information to complete the customs declaration.

The current system used by HMRC for customs declarations; Customs Handling of Import and Export Freight (CHIEF) system, which has been in use since 1994, is being replaced by the Customs Declaration Service (CDS) system.

The current deadlines for the phasing out of CHIEF being available advised by HMRC are 30 September 2022 for imports and 31 March 2023 for exports. Following this CHIEF will cease to operate and the only available system will be CDS.

Why the change?

HMRC are changing the customs declaration system to modernise the customs process as CHIEF entries are based on paper submissions and include several boxes that accept data in a free text format. The CHIEF system was also not designed to manage the volume of customs entries that are now made, and CDS has been designed to ensure that there is a robust system in place that provides a more futureproof solution to increased volumes.

CDS, has been built around data processing rules. As such, most data elements will be restricted to code format other than name and address fields. This means that a higher level of specificity is required, and therefore creates a greater need for accurate details to be provided.

HOW CDS Differs to CHIEF

With this new system, there will come a number of changes that businesses trading internationally should be aware of. These changes will affect the level and type of information that will be requested from you by your Customs Broker.

Data Groups and Data Elements

When making declarations, what are currently known as boxes in CHIEF are being replaced by data elements in CDS. While similar in function they are not like for like, and there will be more data elements required to fill out in CDS than there currently are boxes in CHIEF.

Data elements are categorised into eight data groups. The data group number is used in the identification of the data elements, as an example for dispatch country detail CHIEF box 15 is data element 5/14 in CDS (for data group 5 data element 14). The groups are not necessarily consolidated together in one area on the C88.

Group

Description

Additional detail

1

Message information (including Procedure Codes)

Technical information for HMRC eg entry status such as pre-lodged import. The PCs and APCs for the consignment.

2

References of messages, document, certificates and authorisations

UCR number Licences as required by the commodity code. Authorisation details as dictated by PC and APCs. Proof of origin details if preference is being claimed for duty and VAT reductions.

3

Parties

Details of the parties involved in the consignment’s movement including: Exporter, Importer Declarant, Representative as well as Buyer and Seller. VAT and EORI numbers.

4

Valuation information and taxes

Includes incoterms, invoice value, additions and deduction values for items such as transport costs.

5

Dates, times, periods, places, countries, and regions

Includes dispatch country, destination country, origin country and preference origin country.

6

Goods identification

Includes package details, commodity code, net and gross weights.

7

Transport information (modes, means and equipment)

Includes transport details such as vehicle registration number, trailer number, container number and type of transport across the border.

8

Other data elements (statistical data, guarantees and tariff related data)

Includes financial details such as guarantee type and reference or cash account details if required and type of transaction such as out right sale or financial leasing.

Additional fields for completion:

For import declarations made in CHIEF, up to 68 boxes are typically completed, with 45 boxes completed for export declarations.

In CDS, there will be 91 data elements used across import and export declarations. A subset of 76 data elements may need completing for imports, and 65 for exports, depending on what use the goods are being put to.

A single box in CHIEF can contain several pieces of information; in CDS, the same information may now be separated into specific data elements. For example, box 14 for declarant representative on a CHIEF entry is now made up of 5 data elements on CDS.

CDS also has a mandatory requirement for both net and gross weight of commodities to be entered and therefore both will need to be supplied for every commodity.

Incoterms

Whereas CHIEF only required the letter abbreviation of the incoterm being used for the movement of a consignment. CDS requires the full incoterm to be stated including the named location including country that joins the three letter term for DE 4/1. For example, for an export consignment on FCA terms arranged for collected by the customer on the exporter’s premises in Middlesbrough, that business will need to declare for CDS FCA Middlesbrough, UK or if the terms were CFR for Fremantle, they would need to confirm CFR Fremantle, Australia. An importer on DAP terms to their warehouse in Gateshead would need to state on DAP Gateshead, UK on their declaration instructions.

Customs Procedure Codes

One of the most significant changes to be aware of on CDS will be to do with customs procedure codes (CPCs).

CPCs are used to inform HMRC of the reason for the import/export and identify which Customs regime the goods will enter, such as free circulation or Inward Processing. The CPC also informs HMRC when duties and VAT are to be collected.

On CHIEF, CPCs are comprised of a 7-digit code for each goods item.

On CDS, codes will be split into two parts; a single 4-digit Procedure Code (PC) combined with up to 99, 3-digit Additional Procedure Codes (APCs) for a single goods item.

Much like the changes coming to data elements as detailed above, there is not always a direct conversion between CPC codes on CHIEF, and PC/APC codes on CDS. This is because CHIEF CPC codes are unique to a goods item whereas CDS PC/APC codes make multiple, interchangeable combinations possible that allow a number of circumstances to be represented.

It is the responsibility of the business to provide the relevant PC and APCs for each commodity on every consignment for all customs declarations. Businesses need to familiarise themselves with these new PC/APC codes. Links to HMRC guidance on these new codes can be found via the following links:

*The Correlation Matrices can be used to check which APCs can be used with each PC.

Commodity Codes

Whilst the UK trade tariffs for both CHIEF and CDS were updated at the beginning of 2022 in line with changes made by the World Customs Organisation (WCO). Requirements including for licencing for the same commodity codes in CHIEF and CDS can be different in some instances. Businesses are therefore advised to check the CDS tariff requirements for commodity codes before arranging a CDS declaration. The tariff can be found here.

Getting Access

All traders will need to register for CDS, this can be done via logging into the trader’s Government Gateway Account, where the following pieces of information will need to be provided:

Your EORI number that starts with GB (if you do not have an EORI number starting with GB and are a UK based business, you must apply for one here)

Your Unique Taxpayer Reference (UTR)

The address for your business that matches HMRC’s Customs records

Your National Insurance Number (for individuals or sole traders only)

The date you started your business

Your email address

Once registered for CDS via the Government Gateway traders will be able to view their Financial Dashboard and use the Secure File Upload Service. This will allow supporting payments to be made and supporting documents will be able to be submitted to HMRC such as licenses or certification where required.

Real time account balances and limits can be seen via the Financials page. Limitations are that it will not be possible to view historical transactions against the account.

Changes to payment methods for CDS

Duty Deferment Accounts

To use Duty Deferment Accounts in CDS existing account holders must complete a new Direct Debit Instruction. Original Direct Debit instructions for CHIEF should not be cancelled.

Whilst CHIEF and CDS are both in operation it will be necessary to have two active HMRC Direct Debit Instructions, one for CDS and one for CHIEF, payments for both will be taken on the same day. Separate statements for each account will be issued. This ensures that whilst both systems are operational entries can be made via either system as required.

In CDS deferment account holders will have the option of making interim payments against their deferment account to increase their available balance. This will provide the flexibility to increase the value of declarations in a given month without needing to increase agreed guarantees or limits. Further information is available here.

Any traders using an intermediary to clear goods through UK Customs will need to inform their intermediary of their payment preferences prior to the goods arriving in the UK. Where available as a service, intermediaries will still be able to arrange payment of any VAT and duty via their own Deferment Account on behalf of a trader where agreed by the two parties.

New payment methods on CDS

Flexible Accounting System to become Cash Accounts

The method currently used with CHIEF for payment of VAT and any duties at the time of import clearance will close. The Flexible Account System (FAS) will be replaced by Cash Accounts in CDS. When traders will be automatically issued a Cash Account when they register for CDS. Cash accounts will be managed through the Traders Government Gateway account. When payment is required for a clearance, the Trade will need to ensure that the account has the necessary funds in. Via their Government Gateway account traders will be able to:

Top them up and use them to pay duties due for your goods when at the time the declaration is made

Authorise their agents to use the accounts on their behalf

Use their account in all Customs locations

Allocate funds for declarations to clear against, in chronological order

Withdraw funds from the Cash Account

Further information on paying funds into your CDS Cash Account can be found here.

Traders can view their Cash Account and manage who has permission to use it from the menu option ‘view your customs financial accounts’, which can be accessed via their Government Gateway account.

Immediate Payments

There will also be an option to arrange immediate payments to HMRC for VAT and duty, it will require the import customs clearance reference for that specific clearance to be known at the time of payment.

There are a variety of methods of payments available include CHAPS, BACS, online or telephone banking and debit or corporate credit card.

The 12 digit clearance reference number which will be prefixed with CDSI must be used in conjunction with the correct HMRC bank account details for CDS and the chosen payment method to ensure that the payment is correctly allocated.

Further details on immediate payment options, payment value thresholds and fund clearance timescales can be found here.

Guarantees

If goods are entering a customs special procedure an individual guarantee or a custom comprehensive guarantee may be required. The guarantees are usually required to allow the goods to enter a customs special procedure regime and permit duty to be deferred.

If a traders has a General Guarantee account, permission must be given via the ‘View your customs financial accounts’ on the CDS area of their Government Gateway account to give authorisation for brokers acting on their behalf. General Guarantee Accounts can be used as a combined method of payment with Duty Deferment Accounts.

Further details on General Guarantee accounts is available here.

Where an individual guarantee is used on CDS, it will be possible to use more than one individual guarantee per declaration. The guarantee along with the MRN from the declaration along with the payment reference number will need to be sent to HMRC.

Additional information is available on individual guarantees here.

CDS output document

The output document from CDS will still be called a C88. The C88 generated by CDS will be in a slightly different format to the C88’s generated by CHIEF, due to the changes and additional data fields to be shown on the C88. It will contain all details of VAT and duty costs, unlike CHIEF where additional documents are issued (H2 and E2) to confirm these details.

As with the CHIEF C88, CDS C88’s must be retained as your record of the declaration. HMRC’s requirements for archiving international trade documentation is available here.

Chamber CDS Service and Help

The Chamber has a wide range of services to support businesses with their international trade. The chamber’s ChamberCustoms Brokerage Service and Export Documentation Service are provided by a dedicated team based locally.

ChamberCustoms, the British Chamber of Commerce (BCC) network of agents, are early adopters of CDS and were the first to submit an export declaration via CDS and have been submitting import entries via CDS since November 2021.

If you would like to find out more about our customs brokerage service, please contact [email protected]

For more essential knowledge and guidance to support your international trade, please see the Trade Toolkit section of our website. details of the BCC accredited certificate in international trade module courses, Bitesize knowledge webinars that we run can be found on www.neechamber.co.uk/global.

If you have any queries regarding your international trade or customs declarations or processes please get in touch with the international team on the Global Service Desk via [email protected].

The UK government is planning to unilaterally change it’s border relationship with N. Ireland, which could have significant consequences for UK exporters to the European Union (EU).

Overview Since leaving the EU, the UK-EU has been operating the “Northern Ireland Protocol”. To uphold a borderless Island of Ireland, crucial to the Good Friday Peace Agreement, the Protocol allows goods to flow freely between N. Ireland and the Republic, with checks on goods from Britain.

However, the UK Foreign Secretary, Liz Truss, says the protocol is preventing the formation of N. Ireland’s Government, and diverting GB trade away from Ireland. The Secretary believes the best solution is an EU co-operative one, but without progress, unilaterally plans to drop parts of the Protocol by removing checks on goods between GB-NI, scrapping the sea border.

EU leaders have indicated they will see this act as a lack of good faith, and could impose trade restrictions on UK goods.

Impact on Traders The EU has said “respond with all measures at its disposal” to such a move. This will likely mean tariffs on all UK Exports to the Union, regardless of origin or Trade Agreement preferences. If so, EU importers will have to pay duty on goods from the UK, making UK exports less competitive in EU markets.

Brexit Opportunities Minster, Jacob Rees-Mogg, claims the UK will not retaliate with duties on UK imports from the EU, and it is unlikely there will be any change to the customs process on either side.

CDS

Custom processes between Great Britain and N. Ireland are processed through the new Customs Declaration Service (CDS), a new customs platform coming online for all UK goods in September. The current TSS platform for Irish Movements will be retired by 2024.

ChamberCustoms, the Chamber’s Brokerage service, are early adopters for CDS and can help maintain the smooth flow of your goods with our service based compliance, confidence and clarity.

The UK Government has announced a fourth delay to SPS checks imported into the UK from the European Union, due July 2021, but now expected in Autumn 2023.

Overview

Since our departure from the EU, the UK has slowly implemented a full border between the UK-EU. One of the last processes to be introduced are Sanitary-Phytosanitary (SPS) checks on animal, plant and foodstuff product imports at Border Posts.

Importers will still need to pre-notify the Department for Environment Health Food & Agriculture (Defra) using the IPAFFS system and complete customs processes, while high risk goods, such as live animals, will require full checks.

This will not affect SPS processes on imports from the Rest of the World.

The UK government claim the move is to help with high cost of living crisis and to allow time to implement a smooth and efficient border. Others criticise wasted resources in preparing for the four time delayed border and lack of transparency on how the final process and requirements will look.

Target Models

The Government plans to refresh its “Border Operating Model” in the coming weeks, its overall border strategy, to reflect and include any further changes to the border.

Government also plans to announce a new Target Operating Model this Autumn, expected to layout the roadmap towards “Border 2025”, part of the UK’s ambition to develop a world leading digital and seamless border.

If you are impacted by this, or have any questions, please let us know at: [email protected].

On April 1 2022, the UK government introduced a new plastic packaging tax (PPT), this article aims to inform you on what exactly it is, and what it means for your business.

What is the tax?

The aim of this tax is to incentivise the use of recycled material in the production of plastic packaging. It will affect a very wide range of businesses due to its broad scope. It will affect a multitude of sectors, ranging from consumer goods to cosmetics, pharmaceutical to food and drink, cosmetics to industrial manufacturing and beyond.

This tax will apply at a rate of £200 per tonne on plastic packaging with less than 30% recycled plastic. It will apply to goods manufactured in the UK, as well as packaging on goods which are imported into the UK. This means that if goods don’t meet a minimum of 30% recycled plastic, they will be taxed. If a business exceeds a threshold of 10 tonnes of plastic packaging per annum, further charges will apply.

What do I need to do?

Register

Any business that imports plastic packaging, products contained in plastic packaging, or that manufactures plastic packaging in the UK, will be liable to register for PPT.

Registration is required even if a business does meet the 30% recycled content threshold and in theory does not need to pay any tax.

Businesses can register for Plastic Packaging Tax via the government gateway here, where they can also find a full list of the details required to do so.

How to pay

This tax is paid via the plastic packaging tax return paid to HMRC every quarter. The accounting periods are:

1 April to 30 June

1 July to 30 September

1 October to 31 December

1 January to 31 March

For a more in-depth view of what to include on your plastic packaging tax return, visit the government webpage here.

Keep relevant records

In order to support the information that you submit on your Plastic Packaging Tax return, there are a number of accounts that you must keep in order to prove compliance. A list of the accounts you must keep can be found on this government webpage.

You will also be required to prove that imported or manufactured plastic packaging contains at least 30% recycled plastic, if you intend to avoid the tax. A non-exhaustive list of documents that might be used to prove this is as follows:

Product Specification – which shows proportion of recycled packaging, weight (in tonnes, kilograms, & grams), if packaging is plastic, or if it’s exempt from tax

Contracts – which show the quantity, proportion, and weight of plastic packaging, if packaging is plastic, or if it’s exempt from tax

Production certificates and certificates of conformity – used to show the proportion of recycled plastic in plastic packaging

Business accounting systems – used to show the plastic recycled through the manufacturing process

Accreditations and international standards – Accredited bodies such as the International Organization for Standardization or the British Retail Consortium, conform to a number of standards. HMRC recognises accreditation from organizations such as these.

Quality assurance audits – this can be an internal or external audit that shows the level of recycled plastic, the weight of the plastic packaging, if packaging is plastic, or if it is exempt from tax.

For in-depth and exhaustive instructions on the records and accounts you must keep for PPT, please refer again to the government webpage linked above.

Further Information

On Monday April 25 at 15:45-16:45, there will be an introductory HMRC webinar on the Plastic Packaging Tax. You can sign up to attend it here.

Chamber Services

For more information and support on international trade, please contact the Global Service Desk at [email protected]

Essential knowledge and guidance on all things ‘International Trade’ can be found on the Trade Toolkit section of our website.

Lesley Moody, OBE, President, North East England Chamber of Commerce (AES Digital Solutions) Journal column

After the turbulent times we’ve been experiencing, it’s great to find there’s so much to celebrate in our region at present. Top of the list is the shortlisting of our Durham Culture bid, which is terrific news for us all. Well done to everyone involved! I urge all businesses to pledge their support for the ambitious plans to help bring the title to Durham. The more signatures, the more powerful our submission will be.

We’ve a proud history of celebrating our rich cultural life, reaching back through the centuries, and like everyone in the North East, I’m so excited about the return visit of the Lindisfarne Gospels. They’ll be enjoyed by so many people and add to our tremendous heritage attractions, bringing visitors and investment with them.

In the Chamber we always take pride in our region and all its people. This is particularly true of our female leaders and our recent International Women’s Day event was the perfect opportunity to hear from trailblazing speakers. Emma Gaudern of EMG Solicitors and Sharon Davis from Kasa Communications both have inspirational backgrounds and shared such pertinent advice for the next generation of female entrepreneurs. I’m proud to also play my part as Chamber President.

I’m also an Export Champion and encourage businesses to trade internationally. My own company has provided services around the globe for many years, not without challenges. We’re all starting to get a sense of the EU trading difficulties that remain. The Chamber is working to resolve them while also providing expert advice though our customs and documentation service.

I had the pleasure of hearing about Tees Valley freeport site devolopments recently. I was impressed by director Nolan Gray’s enthusiasm and determination to ensure the whole region’s supply chain benefits from it, and from the red tape reduction that a freeport brings.

With all that’s happening at the moment, I’m pleased to see the Chamber and ChamberCustoms stepping in to provide free documentation to ensure organisations providing humanitarian aid to support Ukraine, are able to do it easily.

My column has had an international flavour, so I want to end by bringing it home and giving a shout out to the Leamside rail line. This investment stretching from Gateshead towards Teesside would be a huge boost to our connectivity for businesses and the wider community, and would start to make levelling up a reality.

The UK has put customs easement in place effective immediately, making it easier to move aid and donations to the people of Ukraine. Border controls and sanitary checks on humanitarian relief have been removed in an attempt to simplify the process. Other formalities have also been removed, such as needing to notify HMRC when the goods have been exported. Read the full press release here and guidance on taking humanitarian aid out of Great Britain to support Ukraine here.

You will no longer need a T1 to export Humanitarian aid out of the UK and French Customs have agreed to allow goods to transit through France without the need of a T1. This now follows the same process as The Netherlands.

The Government still recommends that those who want to help donate cash through trusted charities and aid organisations, such as the Disasters Emergency Committee, rather than donating goods, however. This is because cash can be transferred quickly to areas where it is most needed and can then be used to buy what goods are required.

The easement applies to goods intended to support those affected by the humanitarian crisis in Ukraine which are exported in Great Britain. As long as the goods are not exported to, or through, Russia or Belarus, the simplified processes apply to qualifying goods regardless of destination.

Try to pack goods in groupings of similar items before travelling.

Packing list which will show the weights and list of items travelling

Present your goods movement reference at the port for check-in so you can board.

Vehicles under 3.5 tonnes that carry less than 9 passengers:

You can declare your goods in one of two ways:

Check before setting off if the port or airport has the facilities available to offer oral declarations. If they do, you can declare the goods by speaking to a Border Force officer at the ‘goods to declare’ channel or the red point phone in the customs area at the port or airport.

If there are no facilities available to make an oral declaration, you can declare the goods by taking one of the following actions:

Walking through a customs control point (this can be a green channel signed ‘nothing to declare’) with the goods, if you are on foot

driving (or being driven) past a customs control point with the goods inside your vehicle

Or simply driving through the port if there are no customs control points

You, or the person transporting the goods:

should carry a note of the types of goods

try to pack goods in groupings of similar items before travelling

They may be asked to confirm:

what the goods are

your contact details (or the contact details of the organisation or charity you are moving the goods on behalf of)

the final destination of the goods

But unlike other goods movements, you will not need to supply any customs documentation or get an EORI number to move goods in this way.

The Road Haulage Association is offering to help firms who are trying to move donated goods across borders with customs declarations. They can be contacted at [email protected].

The Chamber and its expert members are supporting regional businesses with their operations to Russia and Ukraine. You can contact us at [email protected]

Below is an updated statement from the Central Bank of Egypt from 13th February on changes to import to Egypt.

As one of the governance procedures to regulate the importation process of goods into Egypt; The decision was made to stop all import transactions through collection of documents and use bank to bank transactions instead.

The only approved way of importing is through letters of credit from importers. This was followed by announcements of exemptions of sectors to the above regulation. The Central Bank of Egypt (CBE) excluded imports of medicines, serums, relevant chemical substances, and some food commodities from the recent decision.

The food items that were excluded include: tea, meat, chicken, fish, wheat, table oil, baby formula, powder milk, bean, lentils, butter, and maize.

The exclusion decision also applies to express mail shipments and shipments that are worth up to $5,000 or an equivalent amount in other currencies.

The CBE has also directed all banks to reduce their commission for opening documentary credits to be equal to the commission paid for collection documents, as not to add financial burdens for the trader.

Please click below to learn more about the new export regulations and the Advanced Cargo Information System.

The Egyptian Consulate has raised its fees for commercial and non-commercial documents. You can find out more here.

We would also like to highlight that the new Advanced Cargo Information System (ACI) will have effect only on Sea shipment transactions, effective from 1st October 2021, NOT on exports by Airfreight and all other modes of shipment; they will be outside the scope of the new measures until new announcements by the Egyptian Government.

The below is taken direct from Egyptian British Chamber of Commerce:

On 5 December 2020, the UK & Egypt signed a new bilateral Trade Agreement. The UK-Egypt Association Agreement provides continued preferential access to both markets and replaces the EU-Egypt Association Agreement from 1 January 2021.

The Chamber promotes trade with Egypt by providing export documentation services for UK exporters to the Egyptian market.

We work closely with all Regional Chambers of Commerce across the UK, as well as the Egyptian Consulate in London to provide a quick and efficient export documentation service.

If you are a UK exporter, you will need to get in touch with your local Chamber of Commerce. The International Trade Department of your Chamber will prepare your export documents and deliver them to us. Once these export documents are fully legalised, we return them to your local Chamber.

The process takes an average of 5 business days. We further offer free express service & amendments for exporters as part of our corporate membership, see Membership

Legal Requirement

Export documentation satisfies the requirements of Customs authorities in Egypt as well as Egypt’s Ministry of Trade & Industry. Ultimately you will not be able to export without the right paperwork; incorrect paperwork can prove costly both in time, money and resource.

Your legalised documents will satisfy your clients in Egypt that the products exported are wholly obtained, produced and/or manufactured in the UK. This verification helps determine the applicable customs tariff.

Furthermore, legalised documents provide assurance to protect you and your product in case of legal disputes.

New Trade Regulations – ACI Pre-Shipment Procedures, binding implementation starts on 1 October 2021

The Egyptian Government has recently issued a new decree aimed at simplifying shipping procedures for export to the Egyptian market. Nafeza – or the National Single Window – uses the CargoX platform which can be used by exporters to submit their shipping documents digitally.

We would like to highlight that these new measures will have effect only on Sea shipment transactions, effective from 1st October 2021, NOT on exports by Airfreight and all other modes of shipment; they will be outside the scope of the new measures until new announcements by the Egyptian Government.

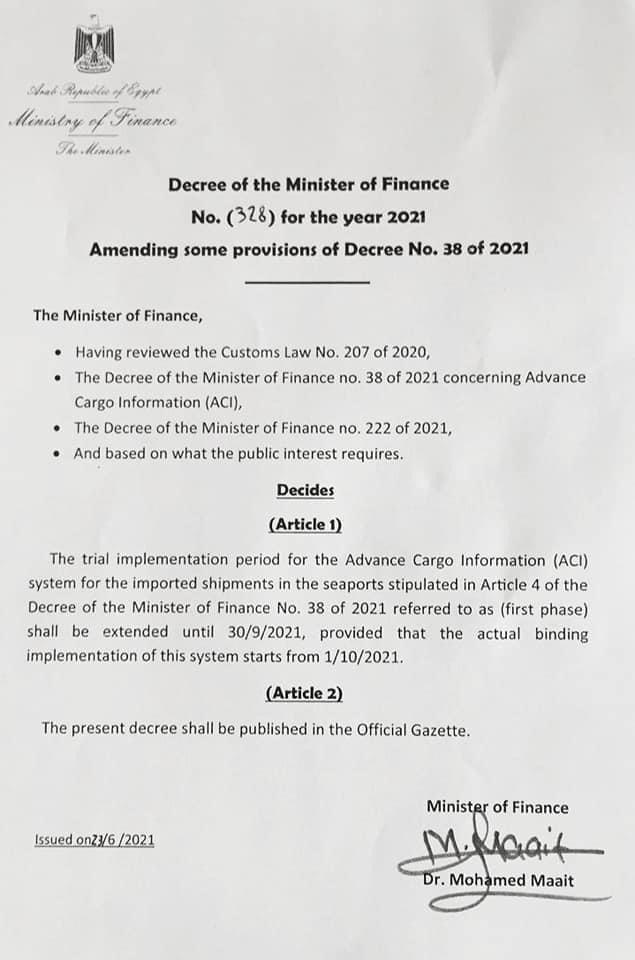

Official Decree 328 for the year 2021: trial implementation period of ACI system is extended until 30/09/21. Binding implementation starts from 01/10/21.

Other Trade Regulations

Since December 2015 it is mandatory for all UK exporters to legalise their Certificate of Origin and have their local Chamber certify the corresponding invoices. The new decrees and regulations are issued by the Egyptian Government, below are the recent changes to regulations for trade with Egypt:

{kind=link}